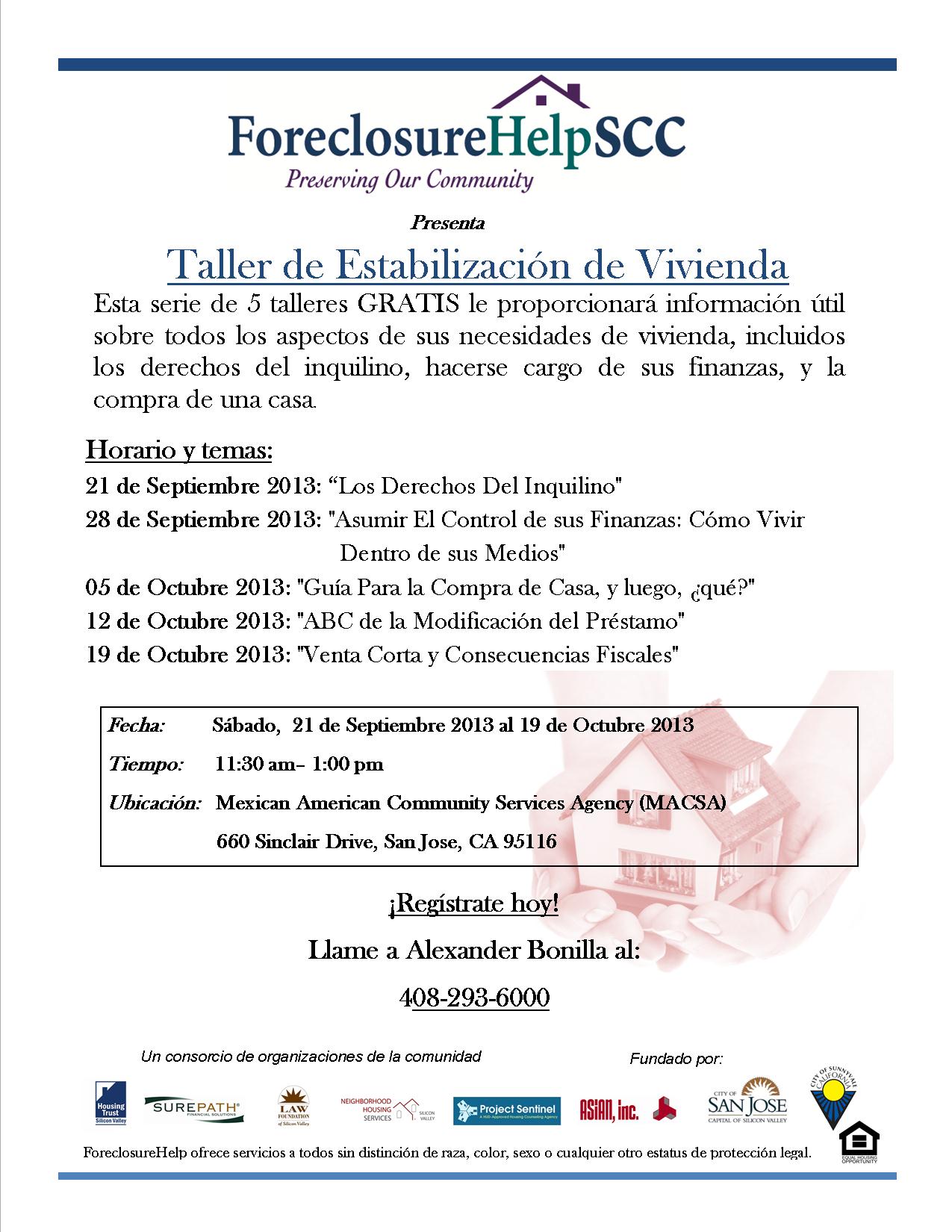

California law prohibits any person or company from collecting advance fees to help negotiate mortgage loan modifications. This law, California Civil Code Section 2944.7, applies to realtors and attorneys. Despite this law, homeowners are still paying thousands of dollars to these scam artists who collect and then fail to perform or even disappear. The lender or servicer holding the mortgage is proceeding with foreclosure, while the homeowner assumes the scam artists are protecting them.

The Santa Clara County District Attorney has actively pursued these law breakers. Two recent cases brought by the DA’s Real Estate Fraud Unit illustrate the harm caused by these illegal practices.

In one case, the co-owners of M & R Contemporary Solutions, pled guilty to theft and foreclosure fraud charges related to a phony scheme that bilked approximately 400 mainly Hispanic homeowners of close to $2 million over a one year period. Homeowners paid fees in the range of $3000 to $10,000 based on promises to save their homes, only to receive no help.

In another case, real estate agent Michael Mendoza was charged with six separate counts of collecting illegal fees and using unlicensed agents. He and his company advertised widely, particularly on Spanish language radio and television stations throughout the Bay Area.

Even though the California law prohibiting advance fees has been in place since 2009, the Foreclosure Help Center continues to receive calls from homeowners who have already paid these illegal fees.

NEVER PAY AN ADVANCE FEE FOR MORTGAGE MODIFICATION OR FORECLOSURE PREVENTION.

Free counseling from a HUD-approved agency is available through the Foreclosure Help Center. Call the Center at 408-293-6000.

If you have paid an illegal advance fee, you can follow up with the District Attorney’s Real Estate Fraud Unit at www.santaclara-da.org.