Preliminary Data Suggests Impact from the Expiration of Mortgage Forgiveness Debt Relief

Is Housing Facing a “Short Sale Cliff”

Reply

Preliminary Data Suggests Impact from the Expiration of Mortgage Forgiveness Debt Relief

Silicon Valley has an image as an economic powerhouse, with high levels of employment and increasing home values. However, the foreclosure rate for the metropolitan area that encompasses Silicon Valley is not noticeably lower than the rates for other areas considered to be hard hit by the foreclosure crisis. A report just released by the Foreclosure-Response organization provides the foreclosure rates for all 366 U.S. Metropolitan areas as of September 2013. Full report. The current foreclosure rate for the San Jose-Sunnyvale-Santa Clara Metro area is 2.3%, which is the same rate calculated for the SF-Oakland Metro area. The Silicon Valley rate is just below the 2.4% rate for Chico, the 2.5% rate for Bakersfield and the 2.7% rate for Sacramento. The rate for Modesto is 3% and Stockton is 3.1%. None of the rates in these hard hit areas are dramatically higher than Silicon Valley.

The report also measured the improvement in the “serious delinquency” rate since the height of the foreclosure crisis in 2009. Serious delinquency is defined as 90 or more days delinquent. The improvement in the delinquency rate in Silicon Valley is actually less than the improvement in other metro areas. The San Jose Metro area serious delinquency rate in December 2009 was 7.8%. It is now 4%. In contrast, the serious delinquency rate for Stockton dropped from 18.5% to 6.1%. In the Modesto Metro area, the delinquency rate fell from 17.3 to 5.8%. As is true in the comparative foreclosure rates, the current delinquency rates in all three of these areas are now similar, contrasting with the sharply higher delinquency rates for these other areas in 2009.

As we all know, the mortgage scam artists constantly invent ways to attract paying customers. Here is a new one to avoid.

Several laws protect homeowners facing foreclosure by requiring lenders and loan servicers to give the homeowner a “single point of contact” within their organizations. This protection is crucial to prevent harmful lender practices such as dual tracking and misplaced modification applications.

We have now learned that profit-motivated third parties are contacting homeowners and leading them to believe they are the point of contact for the lenders and servicers who hold their mortgages. They are asking for private information from the homeowners, and may ultimately ask for fees. As a minimum, this scam activity can confuse homeowners and lead them to waste time that should be spent contacting legitimate representatives.

Homeowners should never deal with someone directly calling who is claiming to be a point of contact.

A legitimate point of contact representative should be identified in an official letter from the lender or servicer, with appropriate contact details included.

This type of scam is another good reason to contact a HUD-approved counseling agency. That agency can communicate with the lender or servicer to verify the point of contact representative and to submit the homeowner’s personal information safely and confidentially. A homeowner who is contacted by one of these scam artists should report the contact to his or her counseling agency, a non-profit legal services agency, or the local district attorney.

The Mortgage Forgiveness Debt Relief Act has been allowed to expire. Before this law was passed in 2007, a homeowner who had a portion of his or her mortgage written off by a lender was considered to have received a taxable benefit equal to the amount of debt forgiven. This rule applied to short sales, some types of modifications, and other forms of foreclosure work out options where a portion of the mortgage debt was waived. As a result, before this Act, a homeowner could lose his or her home and still pay taxes on the amount of the home mortgage that was unpaid. The Mortgage Forgiveness Debt Relief Act waived the taxable status of the event, which has been an important incentive to utilize foreclosure prevention options.

The Act had been routinely extended from 2007 until the end of 2013, but has now been allowed to expire. There are bills pending in congress to re-authorize the Act, and there is another IRS rule for “insolvency” that could protect some of the same transactions. However, every homeowner facing foreclosure should seek advice from a tax professional to address the implications of the expiration of the Act. Many members of the real estate and mortgage industry are not aware of these implications.

For more details, click here,

For a different point of view, see the discussion here,

Here is a summary published by the California Reinvestment Coalition.

Join us this weekend Saturday, September 28th, 2013 at MACSA for our Housing Stabilization Workshop Series! This weeks workshop is titled “Taking over your finances: How to live within your means”. This workshop is FREE to all. There will be light refreshments and snacks. The workshop will be located at 660 Sinclair Drive, San Jose, CA 95116. Please call 408-293-6000 to register!

_____________________________________________

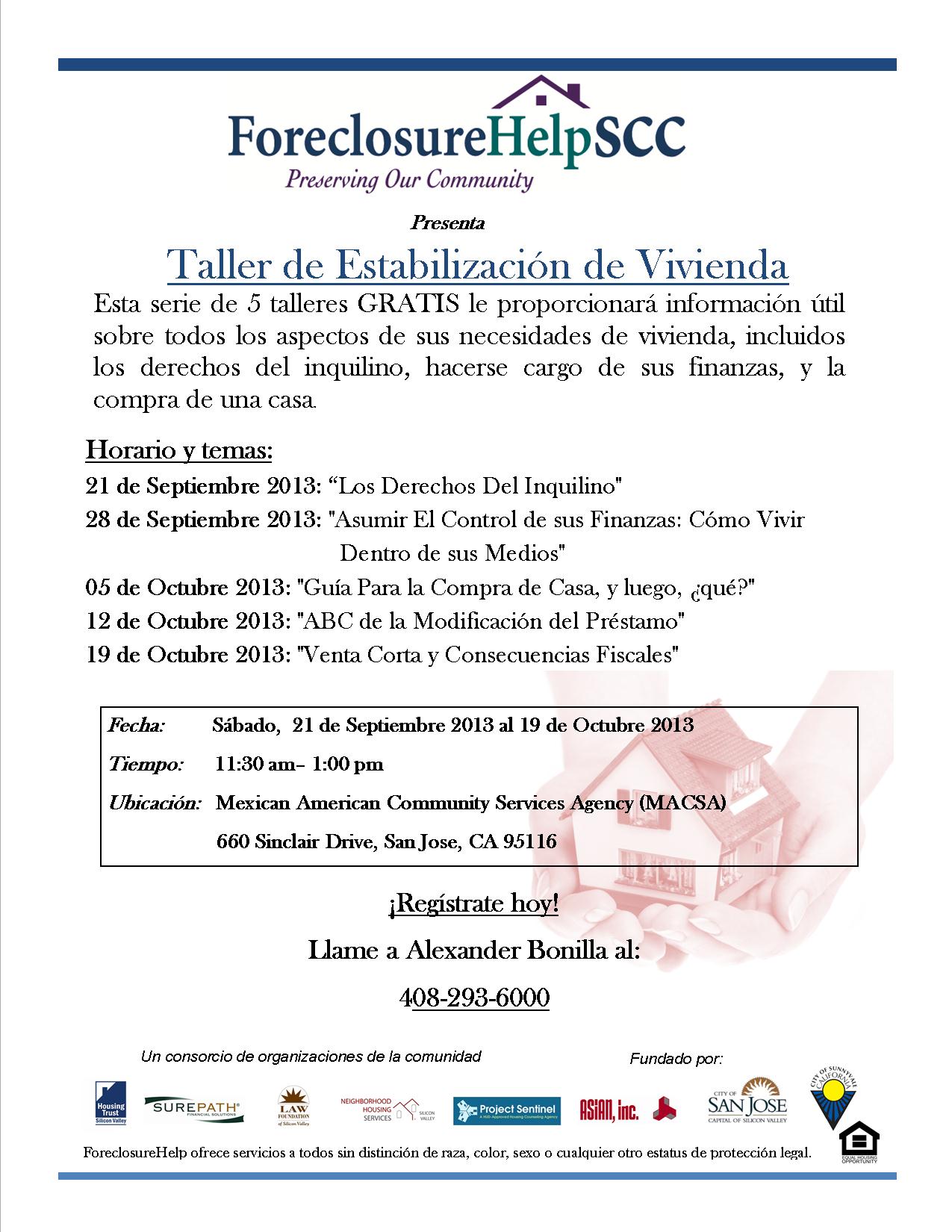

¡Únase a nosotros este fin de semana Sábado, 28 de septiembre 2013 a MACSA para nuestro Taller de Estabilización de Vivienda! Este taller se titula “Hacerse cargo de sus finanzas: ¿Cómo vivir dentro de sus medios”. Este taller es gratuito para todos. Habrá refrescos y aperitivos. El taller se encuentra a 660 Sinclair Drive, San Jose, CA 95116. Por favor llame 408-293-6000 para registrarse!

_____________________________________________

Únase a nosotros este fin de semana Sábado, 28 de septiembre 2013 a MACSA para nuestra vivienda Estabilización Workshop Series! Este taller semana se titula “Hacerse cargo de sus finanzas: ¿Cómo vivir dentro de sus medios”. Este taller es gratuito para todos. Habrá refrescos y aperitivos. El taller se encuentra a 660 Sinclair Drive, San Jose, CA 95116. Por favor llame 408-293-6000 para registrarse!

Esta explicación de la Declaración de Derechos para los Propietarios fue preparada por: El Proyecto Legal de Viviendas Justas.

La Declaración de Derechos para los Propietarios de California by El Proyecto Legal de Viviendas Justas. is licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License. Permissions beyond the scope of this license may be available at www.foreclosurehelpscc.org.

La Declaración de Derechos para los Propietarios de California by El Proyecto Legal de Viviendas Justas. is licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License. Permissions beyond the scope of this license may be available at www.foreclosurehelpscc.org.

La “Declaración de Derechos para los Propietarios” de California (HBOR) agrega nuevas medidas de protección para ayudar a prevenir las ejecuciones hipotecarias evitables. HBOR requiere que los administradores de préstamos y prestamistas provean notificaciones adicionales para que los prestatarios conozcan sus derechos y cómo ponerse en contacto con su administrador de préstamos para obtener una modificación de préstamo u otro tipo de ayuda para prevenir la ejecución.

HBOR impide que “Doble Seguimiento” (“Dual Tracking”) donde los administradores de préstamos ponen a los propietarios en el camino hacia la ejecución hipotecaria, aún cuando se está evaluando una solicitud de modificación de préstamo. HBOR requiere que los administradores brinden un solo punto de contacto consistente para ayudar a los prestatarios durante la evaluación de la solicitud y la ejecución hipotecaria. HBOR también requiere que los prestamistas proporcionen la documentación adecuada antes de que puedan ejecutar la hipoteca, y les dará las herramientas a los prestatarios para que ellos puedan imponer sus derechos.

Antes de archivar una notificación de incumplimiento (NOD), y por lo menos 30 días antes de la inscripción de una NOD, el administrador debe enviar una notificación por escrito al prestatario que indica que si el prestatario es un miembro del servicio militar o dependiente de un miembro del servicio militar, él o ella puede tener derecho a ciertas protecciones. La notificación también debe informar a los prestatarios (tanto militares como no militares) que tienen el derecho de solicitar y obtener documentos fundamentales del préstamo y un historial de sus pagos.

Si el prestamista ya ha archivado una notificación de incumplimiento (NOD), el administrador debe enviar una carta al prestatario dentro de 5 días hábiles después de la inscripción del NOD. La carta debe notificarle al prestatario que él o ella puede ser evaluado/a para una alternativa a una ejecución hipotecaria; declarar si se requiera una solicitud para ser considerado; y describir el proceso por el cual un prestatario puede obtener una solicitud.

Requisitos fundamentales y protecciones bajo HBOR

El Proyecto Legal de Viviendas Justas es miembro de ForeclosureHelpSCC, un programa comunitario que ayuda a los propietarios de viviendas e inquilinos que enfrentan una ejecución hipotecaria. Si usted está enfrentando una ejecución hipotecaria, hay profesionales certificados que pueden ayudarle a entender sus opciones para evitar la ejecución hipotecaria, incluso a través de una modificación de préstamo. Llame a la línea directa: 408-293-6000, visite el sitio web: http://www.foreclosurehelpscc.org, o envíe un correo electrónico: help@foreclosurehelpscc.org.

###

Foreclosure Help is a coalition program funded by the city of San Jose through a HUD Community Development Block Grant and the city of Sunnyvale, and we can directly assist homeowners and tenants in San Jose and Sunnyvale who are facing foreclosure. However, we are unable to assist homeowners/former homeowners in other cities and states. If you need housing counseling, we suggest using the interactive map on HUD’s website.

ForeclosureHelp partners include the Housing Trust Silicon Valley (lead agency), the Fair Housing Law Project at the Law Foundation of Silicon Valley, SurePath Financial Solutions, Project Sentinel, Asian Inc, Neighborhood Housing Services of Silicon Valley, and the Santa Clara County Association of Realtors.

If you are a homeowner living in San Jose or Sunnyvale and are struggling with your mortgage, please contact ForeclosureHelpSCC, a program funded by the City of San Jose through a HUD Community Development Block Grant and the City of Sunnyvale at (408)-293-6000 or visit us: www.foreclosurehelpscc.org Our housing counselors can help you evaluate your options, learn more about federal and state programs that may help you with your mortgage issues, and will help you create a plan forward.

Please note: All content included in the ForeclosureHelpSCC blog is provided for information only and should NOT be considered legal or tax advice. If you have any questions, please feel free to contact us on our hotline: (408)-293-6000, or visit our website: www.foreclosurehelpscc.org or send us an email: help@foreclosurehelpscc.org.

Si usted es dueño de una casa en San José o en Sunnyvale y están luchando con su hipoteca, por favor póngase en contacto con ForeclosureHelpSCC, un programa financiado por la ciudad de San José y la ciudad de Sunnyvale, al (408) -293- 6000, o visite nuestro sitio: www.foreclosurehelpscc.org.

Nuestros consejeros puede ayudarle a evaluar sus opciones, aprender más acerca de los programas federales y estatales que pueden ayudarle con sus problemas de hipoteca, y le ayudará a crear un plan para seguir. Por favor, tenga en cuenta: Todos los contenidos incluidos en el blog ForeclosureHelpSCC se proporciona únicamente a título informativo y no debe ser considerada como consejo legal o fiscal. Si usted tiene alguna pregunta, por favor no dude en contactarnos a nuestra línea directa: (408) -293-6000, o visite nuestro sitio:www.foreclosurehelpscc.org o envíenos un correo electrónico: help@foreclosurehelpscc.org.

Nếu bạn là một sinh hoạt chủ sở hữu nhà ở San Jose hoặc Sunnyvale và đang đấu tranh với nợ nhà, xin vui lòng liên ForeclosureHelpSCC, một chương trình được tài trợ bởi thành phố San Jose và thành phố của Sunnyvale ở (408) -293-6000 hoặc truy cập trang web của chúng tôi: www.foreclosurehelpscc.org.

Nhân viên tư vấn của chúng tôi đã được HUD chấp thuận có thể giúp bạn đánh giá các lựa chọn của bạn, tìm hiểu thêm về các chương trình của liên bang và tiểu bang có thể giúp bạn với các vấn đề thế chấp của bạn, và sẽ giúp bạn tạo ra một kế hoạch phía trước.Xin lưu ý: Tất cả các nội dung trên Blog ForeclosureHelpSCC được cung cấp thông tin duy nhất và không nên coi là hợp pháp hoặc tư vấn thuế. Nếu bạn có bất cứ câu hỏi , xin vui lòng liên hệ với chúng tôi qua đường dây nóng: (408) -293-6000, hoặc truy cập vào trang của chúng tôi: http://www.foreclosurehelpscc.org hoặc gửi email cho chúng tôi:help@foreclosurehelpscc.org. ![]() FAIR HOUSING AND ANTI-DISCRIMINATION POLICY It is the policy of ForeclosureHelp not to discriminate against any person because of that person’s race, color, religious creed, sex (gender), sexual orientation, marital status, national origin, ancestry, familial status (households with children under the age of 18), source of income, disability, medical condition or age. Color or “ethnic group identification” means the possession of the racial, cultural or linguistic characteristics common to a racial, cultural or ethnic group, or the country or ethnic group from which a person or his or her forebears originated. As required by law, we agree to take the affirmative steps needed to further fair housing. ForeclosureHelp will consider any and all requests for reasonable accommodation in the application of its rules, policies, practices, and services, and in the use of its physical structures, in accordance with the requirements of state and federal laws. You can ask ForeclosureHelp to consider any reasonable accommodation you may have. Please consult with the Program Manager (408-293-6000 or via email: help@foreclosurehelpscc.org) to request this accommodation.

FAIR HOUSING AND ANTI-DISCRIMINATION POLICY It is the policy of ForeclosureHelp not to discriminate against any person because of that person’s race, color, religious creed, sex (gender), sexual orientation, marital status, national origin, ancestry, familial status (households with children under the age of 18), source of income, disability, medical condition or age. Color or “ethnic group identification” means the possession of the racial, cultural or linguistic characteristics common to a racial, cultural or ethnic group, or the country or ethnic group from which a person or his or her forebears originated. As required by law, we agree to take the affirmative steps needed to further fair housing. ForeclosureHelp will consider any and all requests for reasonable accommodation in the application of its rules, policies, practices, and services, and in the use of its physical structures, in accordance with the requirements of state and federal laws. You can ask ForeclosureHelp to consider any reasonable accommodation you may have. Please consult with the Program Manager (408-293-6000 or via email: help@foreclosurehelpscc.org) to request this accommodation.

Did you hear the recent news about a homeowner in West Sacramento effectively using the new California Homeowner Bill of Rights to stop foreclosure on his home? You can read about it in the Sacramento Bee: “West Sacramento homeowner uses new state law to stop foreclosure (5/23/2013)” The Fair Housing Law Project at the Law Foundation of Silicon Valley prepared a summary of the California Homeowner Bill of Rights which homeowners can use when working with their bank or servicer to apply for a loan modification.

“How does the California Homeowner Bill of Rights Help You?” by Fair Housing Law Project is licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License. Based on a work at https://foreclosurehelpscc.wordpress.com/2013/06/04/how-does-the-california-homeowner-bill-of-rights-help-you/. Permissions beyond the scope of this license may be available at www.foreclosurehelpscc.org.(Reproducing the text below for commercial purposes is NOT allowed.)

CALIFORNIA HOMEOWNER BILL OF RIGHTS

California’s Homeowner Bill of Rights (HBOR) adds new protections to help prevent avoidable foreclosures. HBOR requires loan servicers and lenders to provide additional notices so that borrowers will know their rights and how to contact their loan servicer to obtain a loan modification or other types of foreclosure relief.

HBOR prevents “Dual Tracking” where loan servicers put homeowners on the foreclosure track, even when a loan modification application is being evaluated. HBOR requires that servicers provide for a single consistent point of contact to help the homeowner through the loan modification and or foreclosure process. HBOR also requires lenders to provide proper documentation before they can foreclose, and it gives borrowers tools to enforce their rights.

Before filing a notice of default (NOD), and at least 30 days prior to recording a NOD, the mortgage servicer must send a written notice to the borrower stating that if the borrower is a service member, or a dependent of a service member, he or she may be entitled to certain protections. The notice must also let borrowers know, (both military and non-military), that they have the right to request and obtain key loan documents, and their payment history.

If the lender has already filed a notice of default (NOD), the mortgage servicer must send a letter to the borrower within 5 business days of recording the NOD, notifying the borrower that he or she may be evaluated for a foreclosure prevention alternative; whether an application is required to be considered; and the process by which a borrower may obtain an application.

Key Requirements and Protections under HBOR

You have 14 days to accept an offered first lien loan modification. If you do not accept the modification, your servicer can proceed with the foreclosure process 14 days after the first lien loan modification is offered.

Loan servicers cannot charge you a fee to apply for a loan modification or other relief.

Late fees cannot be assessed for periods during which a completed loan modification application is under consideration, during an appeal, or while timely loan modification payments are being made.

If you are granted a modification or other relief and the loan is sold or transferred, the subsequent servicer must honor the agreement.

HBOR does not require a servicer to offer you a loan modification if it does not participate in any such program, or if you do not meet the applicable eligibility requirements.

The duty to offer an opportunity to apply for foreclosure prevention alternatives, if available through the lender, is limited to first lien loans.

The Fair Housing Law Project is a member of ForeclosureHelpSCC, a community program that assists homeowners and tenants facing foreclosure. If you are facing foreclosure, there are certified professionals who can help you understand your options to avoid foreclosure, including through a loan modification. Call the hotline: 408-293-6000, visit the website: www.foreclosurehelpscc.org, or send an email: help@foreclosurehelpscc.org

###

Foreclosure Help is a coalition program funded by the city of San Jose through a HUD Community Development Block Grant and the city of Sunnyvale, and we can directly assist homeowners and tenants in San Jose and Sunnyvale who are facing foreclosure. However, we are unable to assist homeowners/former homeowners in other cities and states. If you need housing counseling, we suggest using the interactive map on HUD’s website.

ForeclosureHelp partners include the Housing Trust Silicon Valley (lead agency), the Fair Housing Law Project at the Law Foundation of Silicon Valley, SurePath Financial Solutions, Project Sentinel, Asian Inc, Neighborhood Housing Services of Silicon Valley, and the Santa Clara County Association of Realtors.

If you are a homeowner living in San Jose or Sunnyvale and are struggling with your mortgage, please contact ForeclosureHelpSCC, a program funded by the City of San Jose through a HUD Community Development Block Grant and the City of Sunnyvale at (408)-293-6000 or visit us: www.foreclosurehelpscc.org Our housing counselors can help you evaluate your options, learn more about federal and state programs that may help you with your mortgage issues, and will help you create a plan forward.

Please note: All content included in the ForeclosureHelpSCC blog is provided for information only and should NOT be considered legal or tax advice. If you have any questions, please feel free to contact us on our hotline: (408)-293-6000, or visit our website: www.foreclosurehelpscc.org or send us an email: help@foreclosurehelpscc.org.

Si usted es dueño de una casa en San José o en Sunnyvale y están luchando con su hipoteca, por favor póngase en contacto con ForeclosureHelpSCC, un programa financiado por la ciudad de San José y la ciudad de Sunnyvale, al (408) -293- 6000, o visite nuestro sitio: www.foreclosurehelpscc.org.

Nuestros consejeros puede ayudarle a evaluar sus opciones, aprender más acerca de los programas federales y estatales que pueden ayudarle con sus problemas de hipoteca, y le ayudará a crear un plan para seguir. Por favor, tenga en cuenta: Todos los contenidos incluidos en el blog ForeclosureHelpSCC se proporciona únicamente a título informativo y no debe ser considerada como consejo legal o fiscal. Si usted tiene alguna pregunta, por favor no dude en contactarnos a nuestra línea directa: (408) -293-6000, o visite nuestro sitio:www.foreclosurehelpscc.org o envíenos un correo electrónico: help@foreclosurehelpscc.org.

Nếu bạn là một sinh hoạt chủ sở hữu nhà ở San Jose hoặc Sunnyvale và đang đấu tranh với nợ nhà, xin vui lòng liên ForeclosureHelpSCC, một chương trình được tài trợ bởi thành phố San Jose và thành phố của Sunnyvale ở (408) -293-6000 hoặc truy cập trang web của chúng tôi: www.foreclosurehelpscc.org.

Nhân viên tư vấn của chúng tôi đã được HUD chấp thuận có thể giúp bạn đánh giá các lựa chọn của bạn, tìm hiểu thêm về các chương trình của liên bang và tiểu bang có thể giúp bạn với các vấn đề thế chấp của bạn, và sẽ giúp bạn tạo ra một kế hoạch phía trước.Xin lưu ý: Tất cả các nội dung trên Blog ForeclosureHelpSCC được cung cấp thông tin duy nhất và không nên coi là hợp pháp hoặc tư vấn thuế. Nếu bạn có bất cứ câu hỏi , xin vui lòng liên hệ với chúng tôi qua đường dây nóng: (408) -293-6000, hoặc truy cập vào trang của chúng tôi: http://www.foreclosurehelpscc.org hoặc gửi email cho chúng tôi:help@foreclosurehelpscc.org. ![]() FAIR HOUSING AND ANTI-DISCRIMINATION POLICY It is the policy of ForeclosureHelp not to discriminate against any person because of that person’s race, color, religious creed, sex (gender), sexual orientation, marital status, national origin, ancestry, familial status (households with children under the age of 18), source of income, disability, medical condition or age. Color or “ethnic group identification” means the possession of the racial, cultural or linguistic characteristics common to a racial, cultural or ethnic group, or the country or ethnic group from which a person or his or her forebears originated. As required by law, we agree to take the affirmative steps needed to further fair housing. ForeclosureHelp will consider any and all requests for reasonable accommodation in the application of its rules, policies, practices, and services, and in the use of its physical structures, in accordance with the requirements of state and federal laws. You can ask ForeclosureHelp to consider any reasonable accommodation you may have. Please consult with the Program Manager (408-293-6000 or via email: help@foreclosurehelpscc.org) to request this accommodation.

FAIR HOUSING AND ANTI-DISCRIMINATION POLICY It is the policy of ForeclosureHelp not to discriminate against any person because of that person’s race, color, religious creed, sex (gender), sexual orientation, marital status, national origin, ancestry, familial status (households with children under the age of 18), source of income, disability, medical condition or age. Color or “ethnic group identification” means the possession of the racial, cultural or linguistic characteristics common to a racial, cultural or ethnic group, or the country or ethnic group from which a person or his or her forebears originated. As required by law, we agree to take the affirmative steps needed to further fair housing. ForeclosureHelp will consider any and all requests for reasonable accommodation in the application of its rules, policies, practices, and services, and in the use of its physical structures, in accordance with the requirements of state and federal laws. You can ask ForeclosureHelp to consider any reasonable accommodation you may have. Please consult with the Program Manager (408-293-6000 or via email: help@foreclosurehelpscc.org) to request this accommodation.

The Obama Administration announced today that the HAMP program has been extended until 2015. This is an important development because the program was set to expire at the end of 2013. ForeclosureHelp and our seven partners had signed a letter earlier this year, asking that the program be extended because it has been such an important tool in helping families to remain in their homes.

In the past few months, homeowners have contacted ForeclosureHelp and worked with our certified housing counselors when they’re struggling with their mortgages and possibly facing foreclosure because of a death of a spouse, chronic unemployment, predatory hard money loans, student loans, divorce, etc.

HAMP is an important program that a housing counselor can use to help a homeowner stay in their home. Other programs include Keep Your Home California or Conserva Tu Casa California. The Unemployment Mortgage Assistance Program will pay your mortgage for up to 9 months), HARP, and private, in-house modifications.

A few stats about HAMP from the most recent report on loan modifications in the fourth quarter of 2012:

If you’re a homeowner in San Jose or Sunnyvale, pick up the phone and call ForeclosureHelp today. Our certified counselors can help you analyze your situation, determine which programs may help you (and they’ll assist you to apply) and create a sustainable plan forward.

###

Foreclosure Help is a coalition program funded by the city of San Jose through a HUD Community Development Block Grant and the city of Sunnyvale, and we can directly assist homeowners and tenants in San Jose and Sunnyvale who are facing foreclosure. However, we are unable to assist homeowners/former homeowners in other cities and states. If you need housing counseling, we suggest using the interactive map on HUD’s website.

ForeclosureHelp partners include the Housing Trust Silicon Valley (lead agency), the Fair Housing Law Project at the Law Foundation of Silicon Valley, SurePath Financial Solutions, Project Sentinel, Asian Inc, Neighborhood Housing Services of Silicon Valley, and the Santa Clara County Association of Realtors.

If you are a homeowner living in San Jose or Sunnyvale and are struggling with your mortgage, please contact ForeclosureHelpSCC, a program funded by the City of San Jose through a HUD Community Development Block Grant and the City of Sunnyvale at (408)-293-6000 or visit us: www.foreclosurehelpscc.org

Our housing counselors can help you evaluate your options, learn more about federal and state programs that may help you with your mortgage issues, and will help you create a plan forward.

Please note: All content included in the ForeclosureHelpSCC blog is provided for information only and should NOT be considered legal or tax advice. If you have any questions, please feel free to contact us on our hotline: (408)-293-6000, or visit our website: www.foreclosurehelpscc.org or send us an email: help@foreclosurehelpscc.org.

Si usted es dueño de una casa en San José o en Sunnyvale y están luchando con su hipoteca, por favor póngase en contacto con ForeclosureHelpSCC, un programa financiado por la ciudad de San José y la ciudad de Sunnyvale, al (408) -293- 6000, o visite nuestro sitio: www.foreclosurehelpscc.org.Nuestros consejeros puede ayudarle a evaluar sus opciones, aprender más acerca de los programas federales y estatales que pueden ayudarle con sus problemas de hipoteca, y le ayudará a crear un plan para seguir.

Por favor, tenga en cuenta: Todos los contenidos incluidos en el blog ForeclosureHelpSCC se proporciona únicamente a título informativo y no debe ser considerada como consejo legal o fiscal. Si usted tiene alguna pregunta, por favor no dude en contactarnos a nuestra línea directa: (408) -293-6000, o visite nuestro sitio:www.foreclosurehelpscc.org o envíenos un correo electrónico: help@foreclosurehelpscc.org.

Nếu bạn là một sinh hoạt chủ sở hữu nhà ở San Jose hoặc Sunnyvale và đang đấu tranh với nợ nhà, xin vui lòng liên ForeclosureHelpSCC, một chương trình được tài trợ bởi thành phố San Jose và thành phố của Sunnyvale ở (408) -293-6000 hoặc truy cập trang web của chúng tôi: www.foreclosurehelpscc.org.

Nhân viên tư vấn của chúng tôi đã được HUD chấp thuận có thể giúp bạn đánh giá các lựa chọn của bạn, tìm hiểu thêm về các chương trình của liên bang và tiểu bang có thể giúp bạn với các vấn đề thế chấp của bạn, và sẽ giúp bạn tạo ra một kế hoạch phía trước.Xin lưu ý: Tất cả các nội dung trên Blog ForeclosureHelpSCC được cung cấp thông tin duy nhất và không nên coi là hợp pháp hoặc tư vấn thuế. Nếu bạn có bất cứ câu hỏi , xin vui lòng liên hệ với chúng tôi qua đường dây nóng: (408) -293-6000, hoặc truy cập vào trang của chúng tôi: http://www.foreclosurehelpscc.org hoặc gửi email cho chúng tôi:help@foreclosurehelpscc.org.

![]()

FAIR HOUSING AND ANTI-DISCRIMINATION POLICY

It is the policy of ForeclosureHelp not to discriminate against any person because of that person’s race, color, religious creed, sex (gender), sexual orientation, marital status, national origin, ancestry, familial status (households with children under the age of 18), source of income, disability, medical condition or age. Color or “ethnic group identification” means the possession of the racial, cultural or linguistic characteristics common to a racial, cultural or ethnic group, or the country or ethnic group from which a person or his or her forebears originated. As required by law, we agree to take the affirmative steps needed to further fair housing.

ForeclosureHelp will consider any and all requests for reasonable accommodation in the application of its rules, policies, practices, and services, and in the use of its physical structures, in accordance with the requirements of state and federal laws. You can ask ForeclosureHelp to consider any reasonable accommodation you may have. Please consult with the Program Manager (408-293-6000 or via email: help@foreclosurehelpscc.org) to request this accommodation.

Some of the homeowners from San Jose and Sunnyvale that work with ForeclosureHelp are struggling with their mortgages in part because of medical debt and medical bills. Damaged credit can also be an issue if you’re trying to refinance. This post from the Consumerist highlights recently introduced legislation that would give consumers 120 days to resolve medical debt with collectors before that debt is reported to the credit bureaus.